Most estimates include a total number—but the real risk starts when that number

is not properly broken down into materials, labor, and overhead.

Without a clear, structured process, costs look right on paper but fail when it comes to execution.

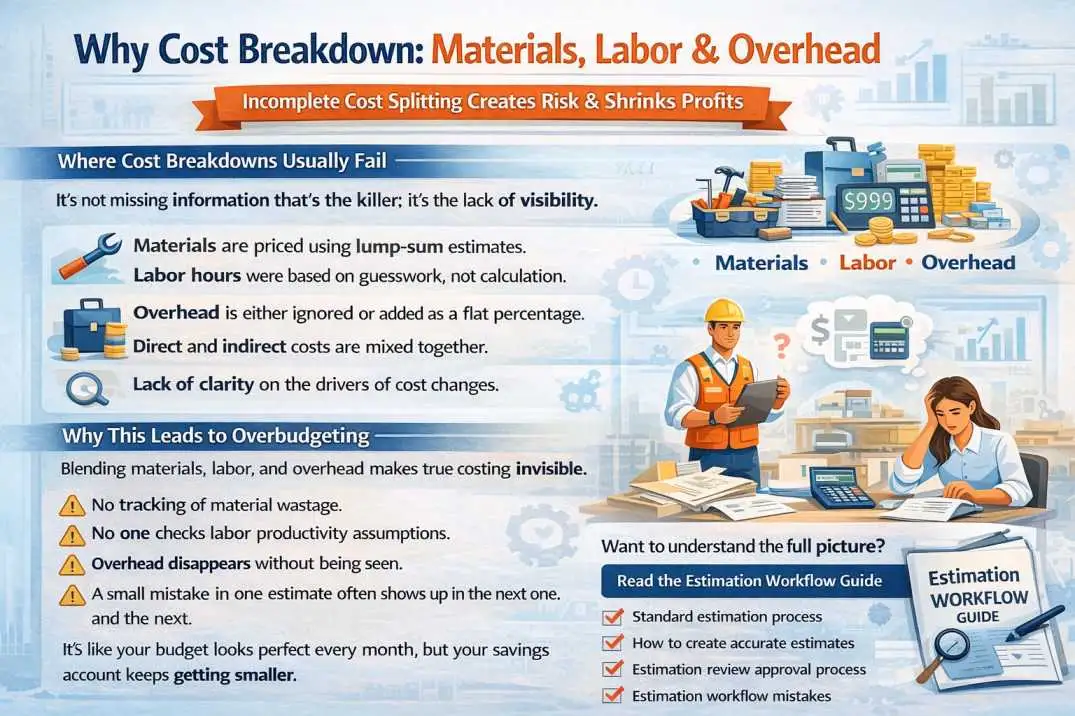

Where Cost Breakdowns Usually Fail

It’s not missing information that’s the killer; it’s the lack of visibility.

- Materials are priced using lump-sum estimates.

- Labor hours were based on guesswork, not calculation.

- Overhead is either ignored or added as a flat percentage.

- Direct and indirect costs are mixed together

- Lack of clarity on the drivers of cost changes.

Important Insight

These cost breakdown problems don’t cause instant damage. They stay hidden until material prices go up, labor runs over, or overhead quietly shrinks your profit.

Why This Leads to Overbudgeting

Blending materials, labor, and overhead makes true costing invisible.

- No tracking of material wastage.

- No one checks labor productivity assumptions.

- Overhead disappears without being seen.

- A small mistake in one estimate often shows up in the next one, and the next.

It’s like your budget looks perfect every month, but your savings account keeps getting smaller.

Why Cost Breakdown Matters: How separating materials, labor, and overhead protects margins and improves estimate accuracy.

How This Problem Is Usually Fixed

Teams that improve cost accuracy introduce:

- We use structured categories for costs: materials, labor, and overhead.

- Standard labor rate calculations.

- Clear overhead allocation rules.

- Line-item level visibility instead of totals.

This turns estimates into decision tools, not just numbers.

Want to understand the full picture?

Read the Estimation Workflow

Read the Estimation Workflow